Essential transfer pricing information for tax agents

Learning Centre • Videos & Webinars • Essential transfer pricing information for tax agents

Learning Centre • Videos & Webinars • Essential transfer pricing information for tax agents

Transfer Pricing is a complex tax area. This video gives a brief overview of what is Transfer Pricing, and what would trigger your need to

see advice from a transfer pricing specialist on behalf of your client.

We currently perform a significant amount of work for second tier/suburban accounting and law firms on a regular basis; those that have no experience with transfer pricing themselves but that want to service their clients and avoid your client using larger firms and potentially losing them.

We make you look good!

With the increasing scrutiny from the Australian Taxation Office (“ATO”) in transfer pricing matters over the recent years, the burden and cost of compliance are taking its toll on taxpayers, particularly, the small to medium businesses.

To all of our accounting firm clients and potential clients, we wanted to alert you to the round of "Failure to lodge" notices that the ATO is now issuing. We recently received one from an accounting firm who as you can imagine, called us in absolute panic! The failure to lodge was for $525,000 penalty!!! Ok, I think I have your attention now!

In 2018, the Inland Revenue Authority of Singapore amended the Income Tax Act to enforce Mandatory Transfer Pricing Documentation for Singapore Taxpayers. Is the new TP Documentation a real game changer?

If you are an Entrepreneur, Start-Up or SMEs don’t disregard transfer pricing and fall under the trap of thinking that transfer pricing affects large MNEs only.

Is your Company subject to transfer pricing in Malaysia? Our article summarises key considerations to ensure compliance with transfer pricing in Malaysia

The challenge has been thrown down. How do we best simplify key points around transfer pricing? We think we’ve found the answer. Pizza. (Stay with us!) If transfer pricing was a pizza, what would be the main ingredients to consider?

The benchmarking analysis is the backbone of a transfer pricing analysis, benchmarking analysis that is reliable and defendable is key when preparing transfer pricing documentation.

Is your benchmarking analysis reliable?

Need a coffee break? Take a five minute and watch #5MinutesTP Episode 4.

Part two about #transferpricing and services transactions, how to price intra-group services

Need a coffee break? Take a break and watch #5MinutesTP Episode 3, #transferpricing for services, trips and traps on how to price services transactions

Do you want to hear from key transferpricing leaders the latest transfer pricing trends? Come and join TPMinds Australia the largest TP Conference in the region.

The Indonesian transfer pricing landscape continues in turmoil, where Companies are struggling to understand and comply with the latest released regulation No. 213/PMK.03/2016 (“PMK-213”).

Lodgement date for CbC Reporting has been extended to February 2018, does your Company need to complete CbC Report, Master File, Local File in Australia?

Unsure on whether your company is pricing services transactions correctly? This article will give key insights on how to price services correctly

Unsure where to start with BEPS Country by Country Reporting? This article explains all you need to know about CbC reporting requirements in Australia.

Good news! Two prestigious awards won - Asia Best Newcomer of the Year and Asia Transfer Pricing Practice Leader of the Year.

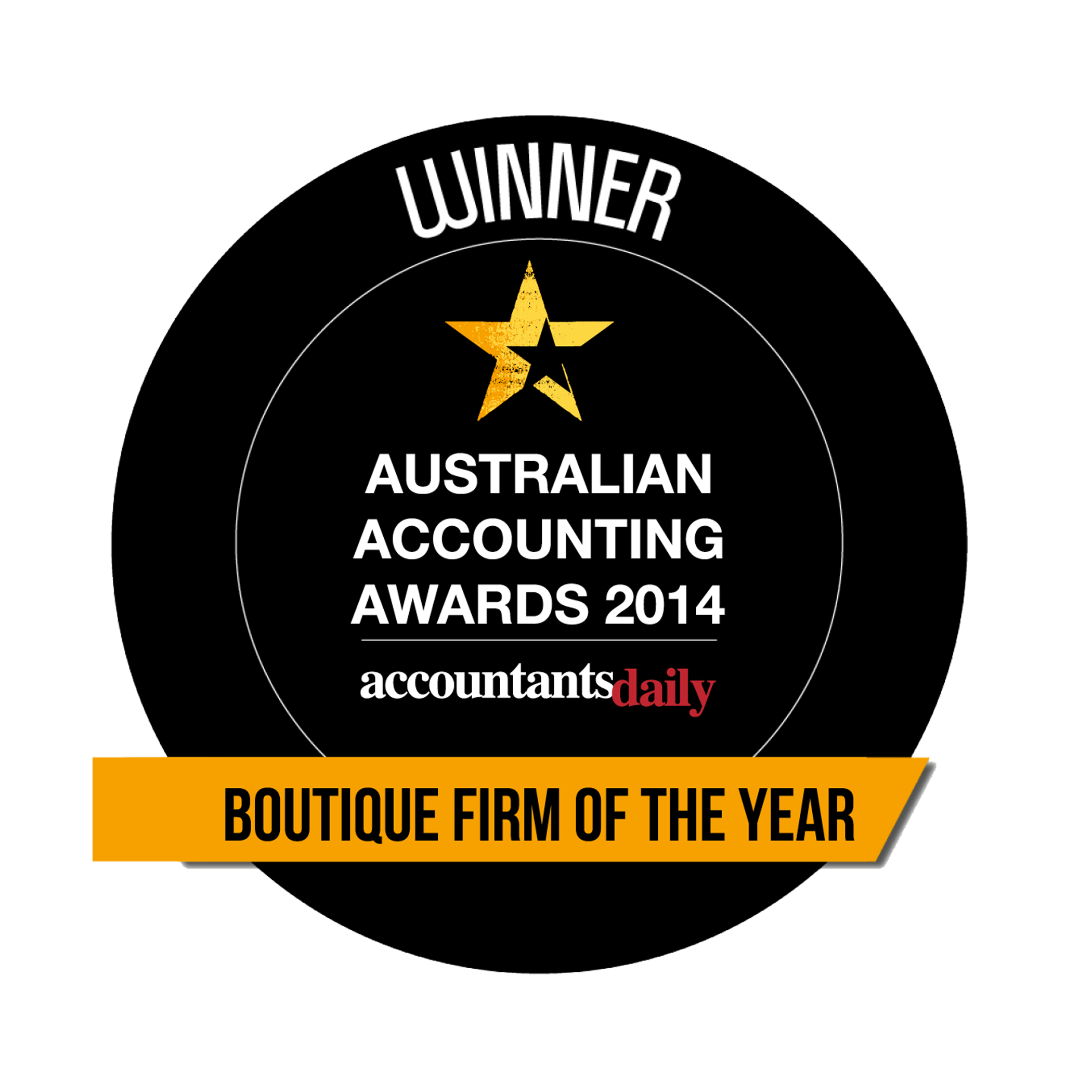

Our nominations for 2017 are Boutique Firm of the Year, Partner of the Year (Boutique) - Shannon Smit, and Thought Leader of the Year - Shannon Smit

Intra-group service transaction is an easy target for transfer pricing adjustment. Two steps to make sure you price them correctly.

Want to know more about how to perform a benchmarking? Read this excellent article published by ISCA Journal, March 2017 edition. Get a copy now, link to article is available in the blog.

New Guidance from the ATO about Australia’s Simplified Transfer Pricing Record Keeping Options, how does it impact your Company?

Australia Transfer Pricing Firm of the Year • Singapore Transfer Pricing Firm of the Year • Best Newcomer of the Year, Transfer Pricing Solutions Asia • Asia Transfer Pricing Practice Leader of the Year, Shannon Smit

Traditionally a preferred transfer pricing method as it is the most direct and reliable way to apply the arm's length principle. But what are the Pros/Cons of applying the CUP method?

On Monday 20 February, the Finance Minister Heng Swee Keat delivered in Parliament Singapore’s 2017 budget. With the tax authorities currently focusing on transfer pricing and the implementation of BEPS action plan, a few of the new measures will impact taxpayers and their related party dealings during 2017.

On January 2016, the ATO released new compliance approach to transfer pricing issues related to centralised operating models (hubs) involving procurement, marketing, sales, and distribution functions. This Practical Compliance Guideline (“PCG”) 2017/1 comes into effect from 1 January 2017 and will apply to existing and newly created hubs.

On 12 January 2017, the IRAS released the 4th edition of its Transfer Pricing Guidelines. We have summarised the key changes that can impact your Company.

The challenge has been thrown down. How do we best simplify key points around transfer pricing? We think we’ve found the answer. Pizza. (Stay with us!) If transfer pricing was a pizza, what would be the main ingredients to consider?

We are honored to be selected among many companies in Singapore to share our story; an excellent read about the human side of transfer pricing and why we love what we do.

We are delighted to announce Shannon Smit, Lead Partner of Transfer Pricing Solutions, as the winner of Partner of the Year – Boutique Firm at the Australian Accounting Awards 2016 organised by Accountants Daily.

As we see the Pokemon Go fever going up around the world, we were interested in knowing why is the world so excited about this game.

We all recovering from the Rio 2016 Olympic Games fever and coping with ‘the Olympic blues’ by following another sportive event or anxiously waiting for the next four years to go by and see our world athletes in Tokyo 2020.

With Australia’s new transfer pricing landscape and BEPS world, intercompany loans are viewed as high risk by Tax Authorities. We have compiled below Frequent Ask Questions from clients that can help you understanding what you need to do to mitigate transfer pricing risks associated with intercompany loans.

With the final reports of the BEPS Action Plan released in October by the OECD and the new transfer pricing documentation standard, a benchmarking analysis that is reliable and defendable is key when preparing transfer pricing documentation.

The Singapore Ministry of Finance announced on 16 June 2016 its commitment and intention to implement the BEPS Action Plan. Singapore will commence a consultation with Multinational Enterprises (MNE) on the implementation of Country By Country (CbC) Reporting and will release details on the outcome in September 2016.

On 15 June 2016, the OECD Council approved the amendments to the ‘Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations’ (Also as the OECD Transfer Pricing Guidelines). The changes are the most significant amendments introduced into the OECD Transfer Pricing Guidelines since 2010.

With transfer pricing gaining so much attention, we have seen an increased interest in accountants wanting to partner with us and outsource part or all of their transfer pricing.

We are delighted to announce Transfer Pricing Solutions as the winner of Australia Transfer Pricing Team of the Year in the Asia Tax Awards 2016 organised by the International Tax Review. The Asia Tax Awards.

The Australia Federal Budget introduced fundamental tax measures that reinforce the Government commitment to tax transparency. Since the released in October 2015 of the final reports from the OECD BEPS Action Plan, Australia has taken significant steps to address the issue of tax avoidance including

On 26 April 2016, The Australian Taxation Office (ATO) released four of Tax Alerts warning multinationals and their tax advisors on potential profit-shifting arrangements that will be closely examining to identify any attempts of tax avoidance.

In the Asia-Pacific Region, Australia, and Japan have both been on the front foot of the BEPS action plan changes releasing legislation to introduce CbC Reporting. It is expected that all countries in the Asia-Pacific Region will introduce the CbC Reporting as it is a key element of the BEPS Action Plan agreed by all 34 OECD member countries, G20 nations, and other nations which joined the BEPS discussions at the OECD.

Transfer Pricing Solutions (TPS) is pleased to reveal a new website to boot!

www.

The CbC Reporting has created a ‘BEPS wave’ in the industry and has become an area of focus for tax practitioners, with many countries releasing new legislation and reporting requirements for multinational enterprises (MNE).

Transfer Pricing Solutions is growing. As an industry leader in the Asia-Pacific Region, we are delighted to announce the opening of our new entity located in Singapore. Transfer Pricing Solutions Asia allows us to cement our expertise in transfer pricing solutions in one of Asia’s largest financial centres, increasing our presence in the region

Transfer pricing remains in the eye of the Australian Taxation Office (ATO) with further developments on the enforcement of Australia’s multinational anti-avoidance law (MAAL). The spotlight on the anti-avoidance law affirms Australia’s commitment to enforcing tax transparency and the implementation of BEPS Action plan.

The ATO is currently focusing on reviewing arrangements involving the use of offshore procurement hubs that source goods on behalf of Australian resident multinational enterprises (MNEs).

In the most recent Tax Payer Alert TA 2015/5, the ATO announced that is focusing on structures where the procurement hub offshore is sourcing goods on behalf of the Australian MNE and is also receiving services from another related party entity located offshore (Service hub).

On 3 December the federal government passed the Tax Laws Amendment (Combating Multinational Tax Avoidance) Bill 2015. The Bill implements the recent guidance set by the OECD as part of its Base Erosion and Profit Shifting (BEPS) initiative with respect to Action Plan 13 by introducing a new transfer pricing standard.

On 26 November the ATO provided further guidance on the application of the STPR options in the form of Frequently Asked Questions (FAQ). In the document, the ATO emphasises on the importance of demonstrating compliance with Australia’s transfer pricing rules, even when applying the STPR options.

We are hearing a lot are having trouble understanding what contemporaneous documentation really means and what are the practical implications. Read our case study as we summarise our experience with the most common misunderstandings.

As published in The Age on 23rd November 2015, the ATO is quoted to take a tighter approach to deal with multinationals on future taxes, meaning agreeing up front in the form of an Advance Pricing Arrangements. The ATO is becoming more ‘picky’ about entering into agreements and has delayed some renewals with major multinationals.

The Chevron case is a big win for the Commissioner and will definitely give confidence to the Australian Tax Office to pursue more transfer pricing cases, although it is expected that with a potential $322 million tax bill, Chevron will appeal.

With conflicting requirements, Year End Financial Statement auditors are in many cases declining to sign off on audits where there is no ‘evidence’, a company has satisfied the new transfer pricing requirements. The quandary for many companies is how to achieve this when transfer pricing documentation is not required to be prepared until approximately 6 months after year end, whilst the auditors come in 2 months after year end.

On September 16 the OECD released guidance on transfer pricing topics as part of the Base Erosion and Profit Shifting (BEPS) Action Plan announced in July 2013. These topics include guidance on Action 13 on transfer pricing documentation and country-by-country reporting.

Intercompany loans continue to be a hot topic and focus point for the Tax Authorities around the world as this type of transactions are considered high risk from a transfer pricing prospective. If your company has entered into intercompany loans it is critical to assess any transfer pricing risk related with the transaction and to have evidence of compliance with the arm’s length principle.

-for-TPS.png)

.jpg)