As one of the most discussed topics, the Global Minimum Tax (“GMT”) is one of the largest tax reformations as part of the initiative under

Pillar 2 of the Base Erosion Profit-Shifting (“BEPS”) 2.0 project. It subjects multinational companies, with an annual revenue of more

than EUR 750 million in minimum 2 out of the past 4 fiscal years, a minimum tax rate of 15% regardless of their location.

The Pillar 2 Model Rules, also known as Global Anti-Base Erosion (“GloBE”) Rules, were released by the OECD on 20 December 2021 to end

the competition between countries to offer the lowest possible corporation tax rates to attract foreign investments by subjecting

multinational groups around the world to a global minimum tax of 15%.

Our goal is to offer a reliable alternative for transfer pricing needs, delivering proactive, practical, and cost-effective advisory services enhanced by cutting-edge technology.

In our upcoming webinar we unpack how global minimum tax connects with transfer pricing, where we are seeing pressure points, and how

tax and finance teams can respond in a practical and cost effective way.

Transfer pricing is a rapidly evolving area of taxation that demands attention from both tax authorities and business leaders. With the challenges of satisfying multiple jurisdictions and managing transfer pricing risks becoming increasingly complex, practical strategies are crucial for success.

With the release of the updated Transfer Pricing Guidelines at the end of last year, 2026 sees tax professionals now turning their attention to what these regulatory updates mean in practice.

The Introduction to Transfer Pricing workshop is designed to arm participants with an understanding of transfer pricing as well as transfer pricing compliance in various Asia Pacific countries. In addition, a discussion of the various transfer pricing methods and their application, as well as the transfer pricing regime in Singapore will be presented.

Across Asia-Pacific, multinational groups are facing increasing complexity as tariff measures and transfer pricing rules begin to overlap more directly.

US‑based multinational enterprises (MNEs) will continue to be subject to Singapore’s Qualified Domestic Minimum Top-Up Tax (QDMTT), even though they may not be subject to a top‑up tax under US rules.

Starting May 2026, in-scope multinational enterprise (MNE) groups must register for Singapore’s Multinational Enterprise Top-up Tax (MTT), Domestic Top-up Tax (DTT), and the GloBE Information Return (GIR) under the Multinational Enterprise (Minimum Tax) Act 2024.

For the year 2026, IRAS has updated its indicative margin, reaffirming its support for simplified, arm’s length transfer pricing practices.

Singapore taxpayers entering into financial arrangements with related parties must ensure compliance with the arm’s length principle. This includes transactions such as cash pooling, hedging, financial guarantees, captive insurance, and related party loans.

Join us in this workshop as we delve into real-life case studies to share practical knowledge on managing transfer pricing in Singapore and the Asia Pacific region.

We’re thrilled to announce that Transfer Pricing Solutions Asia (Singapore) and Transfer Pricing Solutions Malaysia have both been ranked as recommended Transfer Pricing firms in the 2026 ITR World Tax rankings.

We’re proud to announce that Transfer Pricing Solutions Australia has been ranked as a Tier 2 firm in Transfer Pricing in the prestigious 2025 ITR World Tax rankings solidifying our position among the leading transfer pricing advisory firms in the country.

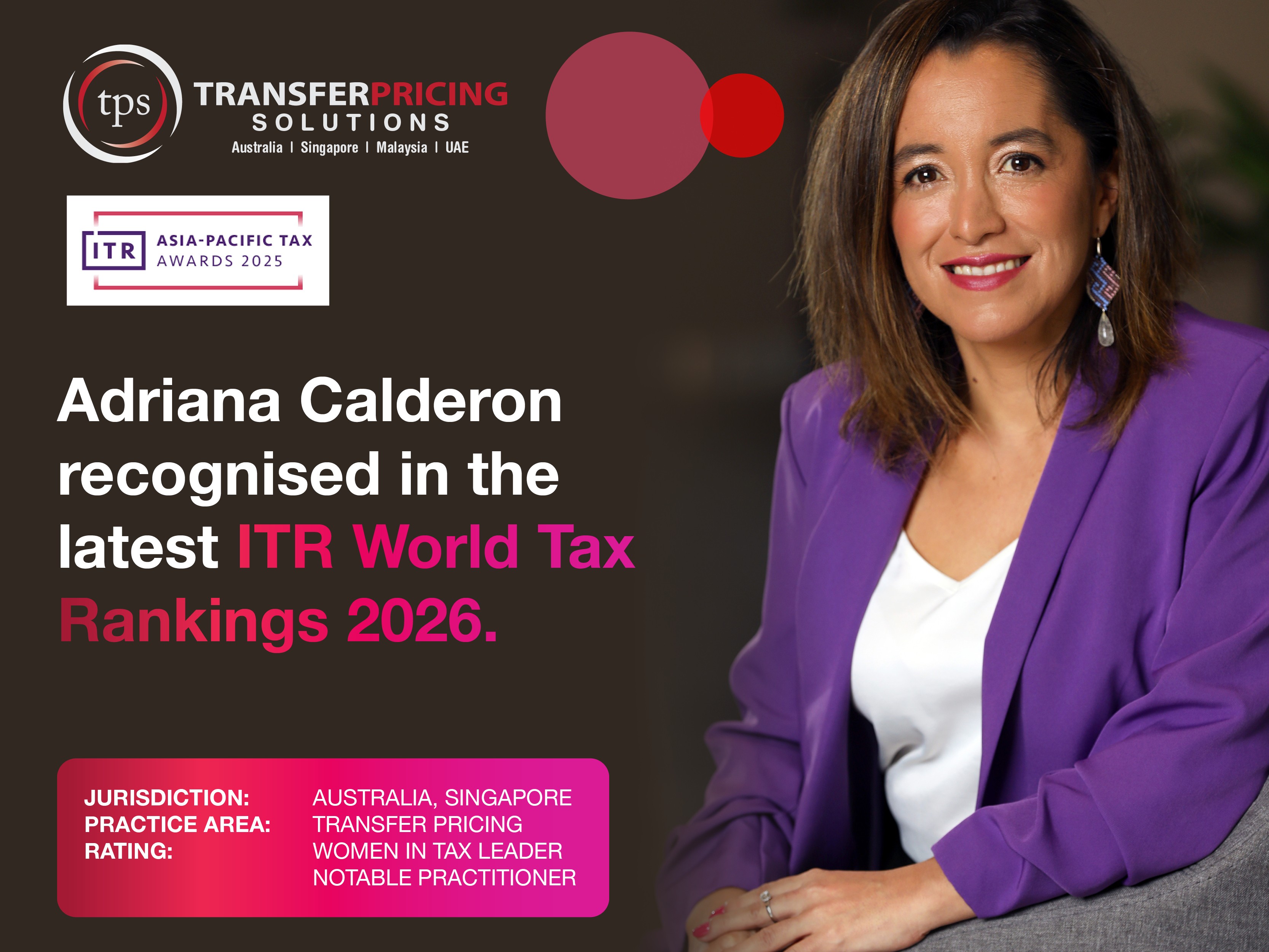

We’re delighted to share that Adriana Calderon, Director and Co-Founder of Transfer Pricing Solutions Asia, has been named a Women in Tax Leader and Notable Practitioner in the 2026 ITR World Tax rankings for the Singapore jurisdiction. In addition, Transfer Pricing Solutions Asia and Malaysia have both been ranked as recommended Transfer Pricing firms.

We're proud to announce that our Founder and Director, Shannon Smit, has been recognised as a Highly Regarded Transfer Pricing specialist and Women in Tax Leader for the Australia jurisdiction in the 2026 ITR World Tax Rankings. In addition, Transfer Pricing Solutions Australia has been ranked as a Tier 2 transfer pricing firm.

This workshop aims to provide actionable insights and tools for finance professionals, tax advisors, and business leaders to effectively manage transfer pricing within their respective industries.

The Introduction to Transfer Pricing workshop is designed to arm participants with an understanding of transfer pricing as well as transfer pricing compliance in various Asia Pacific countries.

This webinar will provide you with the top practical tips for success! We’ll discuss best practices for intragroup financing in the region, including regulatory and risk management issues and potential pitfalls.

Multinationals in Asia are navigating new tax regimes and compliance requirements. New OECD rules on international tax have propelled Asia to the forefront of one of the most significant international tax reforms in decades.

WEBINAR 25 September

Transfer pricing rules for intra-group loans are becoming more scrutinised in Singapore and Asia. Staying compliant while managing risk

effectively is essential for businesses operating across borders.

Winning the 2025 ITR Asia-Pacific Tax Award in Transfer Pricing isn’t just a win for us - it’s a win for businesses across Australia and the APAC region.

Our expert speakers will discuss the latest trends in intra-group services in Malaysia and offer advice on how to develop effective management strategies.

This webinar aims to provide participants across Singapore and Asia with a comprehensive understanding of the Global Minimum Tax (GMT) framework.

Navigating Malaysia’s updated transfer pricing landscape requires more than a basic understanding. With two major transfer pricing guidelines now totalling over 180 pages (excluding appendices), businesses with cross-border activity between Singapore and Malaysia must be ready to adapt, act, and comply confidently.

While much of the public discourse on tariffs has been dominated by political headlines, the business reality is far more complex—and far-reaching.

With tariff volatility on the rise—particularly in US-bound trade—businesses across Asia are facing a new set of challenges that directly impact profitability, supply chain design, and transfer pricing policies.

This webinar is designed to equip you with clear, practical guidance on Singapore’s latest transfer pricing rules, including key documentation requirements and IRAS expectations.

Join us for an immersive day of learning alongside leading experts as they unravel key global trends and, crucially, deliver specific, actionable local and regional insights.

A 60‑minute expert-led webinar explaining how tariff volatility intersects with arm’s‑length transfer pricing requirements and intercompany policy design.

A 60‑minute expert-led webinar explaining how tariff volatility intersects with arm’s‑length transfer pricing requirements and intercompany policy design.

To assist taxpayers in complying with new minimum tax requirements, the ATO has released Draft Practical Compliance Guideline PCG 2025/D3, which outlines a practical administrative approach to penalty enforcement during a crucial transition period.

Malaysia’s Transfer Pricing Guidelines have been comprehensively updated. Join our expert led webinar to understand what’s changed, why

it matters, and how to respond with confidence. Presented in Chinese by Mr Bing Jing Yam.

馬來西亞的移轉訂價指引已進行全面更新。參加我們由專家主導的線上研討會,了解有哪些變更、為何重要,以及如何自信應對。由嚴秉進先生以中文主講。

Malaysia’s Transfer Pricing Guidelines have been comprehensively updated. Join us to understand what’s changed, why it matters, and how to respond with confidence.

Transfer Pricing Solutions Malaysia has been announced as a finalist for Transfer Pricing Firm of the Year – Malaysia in the 2025 ITR Asia-Pacific Tax Awards.

Transfer Pricing Solutions has been named a finalist in the prestigious 2025 ITR Asia-Pacific Tax Awards in three key jurisdictions: Australia, Singapore, and Malaysia, under the category of Transfer Pricing Firm of the Year.

Transfer Pricing Solutions Asia has been shortlisted as a finalist for Transfer Pricing Firm of the Year – Singapore in the 2025 ITR Asia-Pacific Tax Awards.

Gain practical clarity and confidence in preparing the International Dealings Schedule (IDS) with this insightful session, designed to simplify compliance and reduce risk.

This webinar aims to provide participants with a foundational understanding of transfer pricing principles, global standards, and their importance in intercompany transactions.

From 1 January 2025, the ATO is updating its Local File reporting requirements for CbCREs. These changes aim to enhance clarity, consistency, and compliance across international tax reporting.

Starting 1 July 2024, certain large multinational enterprises (MNEs) will be required to publicly disclose select tax and operational data under the new Public Country-by-Country (CBC) Reporting regime in Australia.

Factors to consider when determining the amount of your inbound, cross-border related party financing arrangement - ATO compliance approach

As global tax reform reshapes the way multinationals manage cross-border transactions, Operational Transfer Pricing (OTP) is rapidly becoming a business-critical priority, especially in the Asia-Pacific (APAC) region.

As global trade becomes more complex, companies are re-examining their supply chains - and transfer pricing is at the heart of that conversation.

The OECD has published updated transfer pricing country profiles reflecting the current transfer pricing legislations and practices of 11 jurisdictions and issued for the first time the profiles of Azerbaijan and Pakistan. These latest country profiles present country-specific information on the transfer pricing treatment of hard-to-value intangibles and the simplified and streamlined approach for baseline marketing and distribution activities.

This session will delve into the significance of withholding tax when dealing with international payments.

Learn the latest Singapore & Asia-Pacific transfer pricing trends. Update policies, manage risks.

In multinational enterprises, it is common for parent companies or group service companies to provide intra group services to related parties. These services are outsourced to the group service provider for business convenience and efficiency reasons.

Malaysian Taxpayers who use the 5% markup concession are still required to prepare documentation to address other fundamentals aspects of a service charge.

Transfer pricing refers to the pricing of transactions between related parties, such as sales of goods, provision of services, or financial arrangements. To ensure these transactions are conducted at arm’s length, the Inland Revenue Board of Malaysia (IRBM) requires taxpayers to prepare Transfer Pricing Documentation (TPD).

Comprising all of 180 pages long excluding appendices, the TP guide certainly has gotten the attention of many businesses and the tax community, both in Malaysia and Singapore.

From 1 January 2025 to 31 December 2034, companies operating in qualifying sectors can apply to the Malaysian Investment Development Authority (MIDA) for the various tax incentive schemes under the JS-SEZ Tax Incentives Package.

This webinar is designed to provide participants with practical strategies and insights for managing the complexities of intragroup financing in Malaysia.

Comprising all of 180 pages long excluding appendices, the TP guide certainly has gotten the attention of many businesses and the tax community, both in Malaysia and Singapore.

One of the hottest topics this month is the Special Economic Zone in Johor jointly run by Malaysia and Singapore that will see the creation of 20,000 skilled jobs in the first five years.