The Australian Taxation Office (ATO) has introduced Public Country by Country Reporting (Public CbCR), that requires certain large

Multinational Enterprises (MNEs) to publicly disclose tax and financial information for every country in which they operate, published on a

publicly accessible government website.

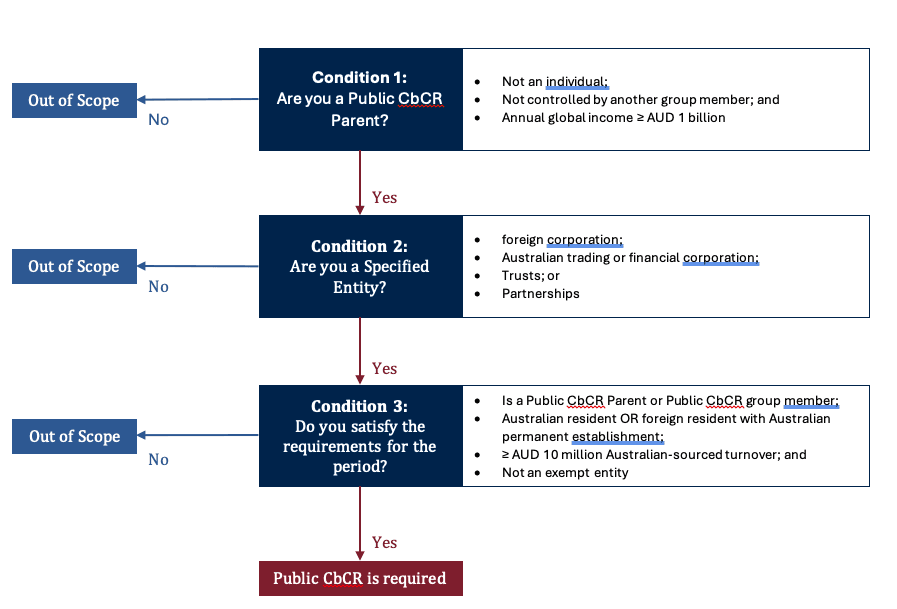

Eligibility Large

MNEs must lodge Public CbCR if it meets 3 main conditions, these are summarised in the figure below:

The introduction of Australia’s Public Country‑by‑Country Reporting regime represents a significant shift in how large multinational

groups are expected to demonstrate tax transparency. Unlike OECD CbCR, Public CbCR requires detailed country‑level tax and financial

information to be published on a government website, placing groups under increased regulatory, media and stakeholder scrutiny.

For in‑scope MNEs, the challenge extends well beyond data collection. Public disclosures must be internally consistent with transfer

pricing documentation, statutory accounts, ESG reporting and public statements, with any misalignment potentially creating reputational or

compliance risk. Early preparation, robust governance and a clearly documented reporting methodology are critical to managing the

operational complexity and public exposure that come with this new reporting obligation.

Prepare with Confidence for Public CbCR

Strengthen governance and alignment under Public CbCR.

.jpg)