EN | CN

All you need to know about transfer pricing documentation.

The Berry Ratio may sound light‑hearted, but in transfer pricing it is one of the most debated Profit Level Indicators (PLIs) used under the Transactional Net Margin Method (TNMM). Simple in formula yet demanding in application, the Berry Ratio continues to attract scrutiny from tax authorities worldwide.

Geopolitical volatility has moved from the margins of risk management to the centre of transfer pricing strategy. For multinational groups operating across Australia, Asia and Europe, geopolitical turmoil is no longer a short-term disruption to be explained away in annual documentation.

Singapore’s Budget 2026 sets out a clear strategy to strengthen competitiveness in a changing global environment. The Budget introduces important tax measures while confirming Singapore’s implementation of OECD Pillar Two global minimum tax rules.

Across Asia-Pacific, multinational groups are facing increasing complexity as tariff measures and transfer pricing rules begin to overlap more directly.

US‑based multinational enterprises (MNEs) will continue to be subject to Singapore’s Qualified Domestic Minimum Top-Up Tax (QDMTT), even though they may not be subject to a top‑up tax under US rules.

Starting May 2026, in-scope multinational enterprise (MNE) groups must register for Singapore’s Multinational Enterprise Top-up Tax (MTT), Domestic Top-up Tax (DTT), and the GloBE Information Return (GIR) under the Multinational Enterprise (Minimum Tax) Act 2024.

For the year 2026, IRAS has updated its indicative margin, reaffirming its support for simplified, arm’s length transfer pricing practices.

Singapore taxpayers entering into financial arrangements with related parties must ensure compliance with the arm’s length principle. This includes transactions such as cash pooling, hedging, financial guarantees, captive insurance, and related party loans.

We’re thrilled to announce that Transfer Pricing Solutions Asia (Singapore) and Transfer Pricing Solutions Malaysia have both been ranked as recommended Transfer Pricing firms in the 2026 ITR World Tax rankings.

We’re proud to announce that Transfer Pricing Solutions Australia has been ranked as a Tier 2 firm in Transfer Pricing in the prestigious 2025 ITR World Tax rankings solidifying our position among the leading transfer pricing advisory firms in the country.

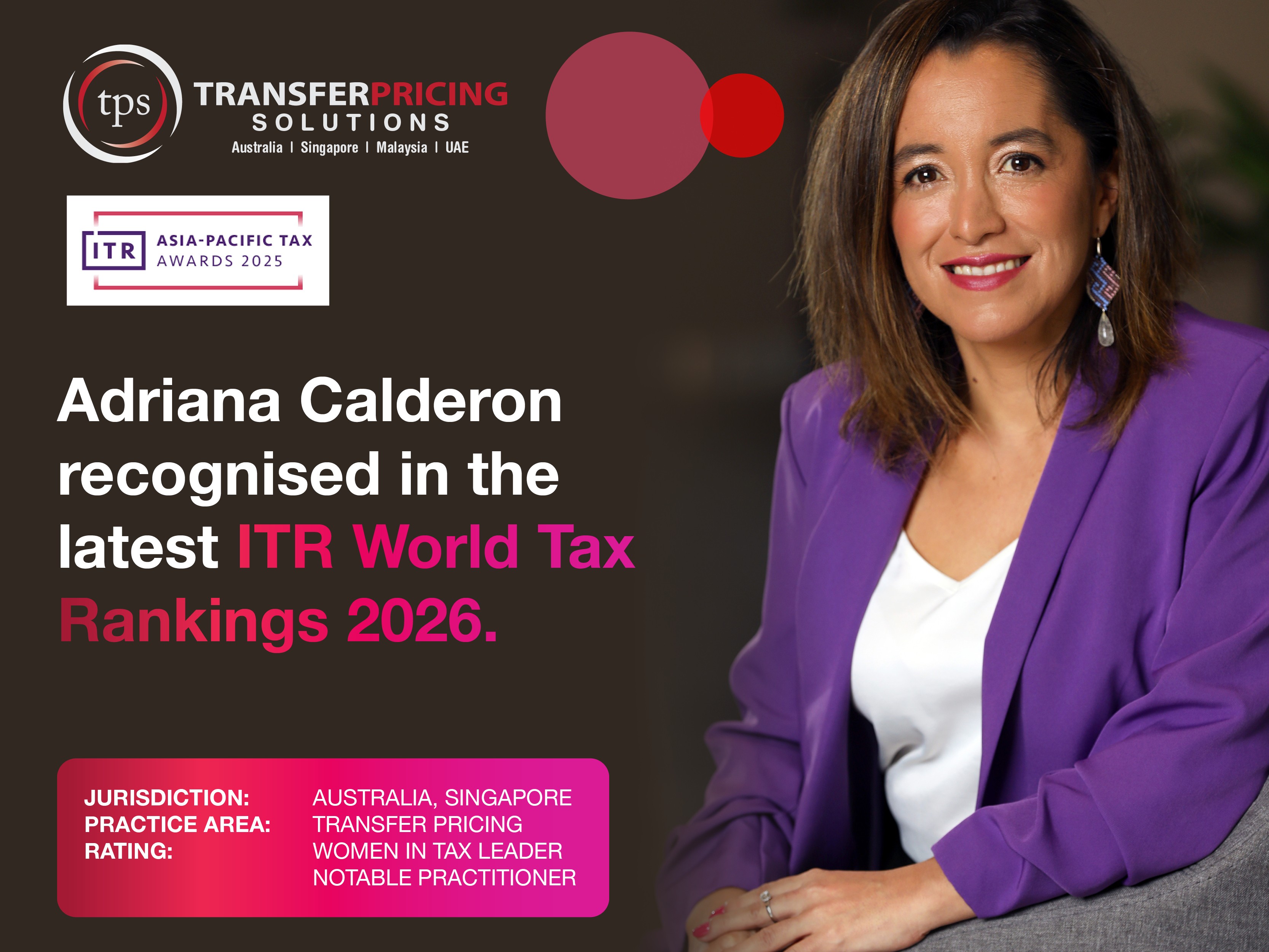

We’re delighted to share that Adriana Calderon, Director and Co-Founder of Transfer Pricing Solutions Asia, has been named a Women in Tax Leader and Notable Practitioner in the 2026 ITR World Tax rankings for the Singapore jurisdiction. In addition, Transfer Pricing Solutions Asia and Malaysia have both been ranked as recommended Transfer Pricing firms.

We're proud to announce that our Founder and Director, Shannon Smit, has been recognised as a Highly Regarded Transfer Pricing specialist and Women in Tax Leader for the Australia jurisdiction in the 2026 ITR World Tax Rankings. In addition, Transfer Pricing Solutions Australia has been ranked as a Tier 2 transfer pricing firm.

Multinationals in Asia are navigating new tax regimes and compliance requirements. New OECD rules on international tax have propelled Asia to the forefront of one of the most significant international tax reforms in decades.

Winning the 2025 ITR Asia-Pacific Tax Award in Transfer Pricing isn’t just a win for us - it’s a win for businesses across Australia and the APAC region.

With tariff volatility on the rise—particularly in US-bound trade—businesses across Asia are facing a new set of challenges that directly impact profitability, supply chain design, and transfer pricing policies.

Transfer Pricing Solutions Asia has been shortlisted as a finalist for Transfer Pricing Firm of the Year – Singapore in the 2025 ITR Asia-Pacific Tax Awards.

As global tax reform reshapes the way multinationals manage cross-border transactions, Operational Transfer Pricing (OTP) is rapidly becoming a business-critical priority, especially in the Asia-Pacific (APAC) region.

As global trade becomes more complex, companies are re-examining their supply chains - and transfer pricing is at the heart of that conversation.

The OECD has published updated transfer pricing country profiles reflecting the current transfer pricing legislations and practices of 11 jurisdictions and issued for the first time the profiles of Azerbaijan and Pakistan. These latest country profiles present country-specific information on the transfer pricing treatment of hard-to-value intangibles and the simplified and streamlined approach for baseline marketing and distribution activities.

In multinational enterprises, it is common for parent companies or group service companies to provide intra group services to related parties. These services are outsourced to the group service provider for business convenience and efficiency reasons.

Malaysian Taxpayers who use the 5% markup concession are still required to prepare documentation to address other fundamentals aspects of a service charge.

From 1 January 2025 to 31 December 2034, companies operating in qualifying sectors can apply to the Malaysian Investment Development Authority (MIDA) for the various tax incentive schemes under the JS-SEZ Tax Incentives Package.

The Johor-Special Economic Zone (JS-SEZ) is a strategic initiative between Singapore and Malaysia aimed at fostering cross-border economic growth.

Since 2017, the Inland Revenue Authority of Singapore (IRAS) has provided indicative margins to help businesses determine an arm’s length interest rate for related party loans. In this article we example the margins.

As of January 1, 2025, new amendments to Singapore's Transfer Pricing (TP) regulations will impact how intra-group loans are handled—specifically for domestic financing arrangements. These updates introduce significant changes that businesses must consider to ensure compliance and avoid potential tax penalties. Here’s what you need to know.

The long-awaited Malaysia Transfer Pricing Guidelines 2024 are finally here, and they bring significant updates aimed at enhancing clarity, compliance, and alignment with global practices. Here’s a breakdown of the key changes every business should know.

Misalignments with regulations, discrepancies in data, and evolving interpretations of arm's length principles can all trigger disputes, potentially leading to significant financial implications.

This article will provide an overview of what global minimum tax is, why it's important, and how it impacts multinational corporations and the global economy.

This article will explore the history of global minimum tax policies, from their origins to the latest developments, including the recent OECD/G20 agreement.

This article will discuss how technology can help multinational corporations streamline their global minimum tax compliance.

This article will discuss how global minimum tax policies affect multinational corporations, including changes to their tax planning strategies and compliance requirements.

This article will provide an overview of the legal and regulatory considerations that multinational corporations need to be aware of when dealing with global minimum tax.